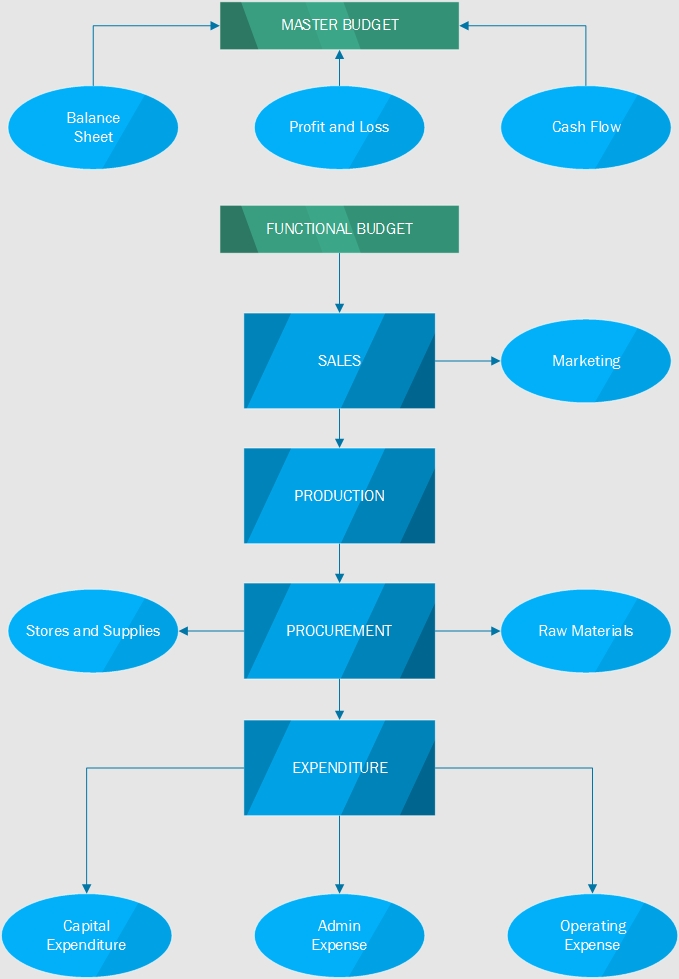

INTRODUCTION

It is a quantitative plan for acquiring and using resources over a time period. Actual spending compared to the budget to make sure the plan is being followed. Individuals create household budgets for their income and expenditures for food, clothing, housing, and so on. Negotiation is crucial to determine whether budget becomes an effective tool or just a clerical exercise.

Every company must make decisions related to the products and services that it sells. For example, each year Procter & Gamble must decide how to allocate its marketing budget across 23 brands that each generates over $1 billion in sales.

POLICY AND GUIDANCE

Helps managers how they should respond to any expected changes like.

- Economic scenario and inflation

- Focus on competitor strategies

- Expected price changes

- Increase market share

- Expected market growth

- Expansion of production

- Increase market share

- Any change in product demand

CORPORATE PLANNING AND BUDGETING

- Designed for a desired future and of effective ways of implementing it.

- Long term plans extending beyond one year – say three to five years.

- Concerned with implementation of long term plan for the year ahead.

- An integrated part of long term planning.

MULTIPLE FUNCTIONS OF BUDGET

- Planning annual operations.

- Coordinating budget activity.

- Communicating plans to various responsibilities center.

- Motivating personal to strive to achieve organizational goals.

- Evaluating performance of managers.

COORDINATION

Managerial decisions involve several functions i.e. marketing, production, commercial; finance and human resource. Co-ordinate various inter related aspects of decision making, otherwise, manager makes wrong decisions.

For instance:

- Marketing starts promotional campaigns to increase sales demand without considering existing production resources.

- Inconsistent production schedule creating problem to sales and marketing to meet budgeted sales.

- Production facilities not enhanced due to limited finance resources.

- Limited availability of raw materials and no arrangements of substitute materials.

STRATEGIC DECISIONS (Insistences)

Southwest Airlines must decide what ticket prices to establish for each of its thousands of flights per day. General Motors must decide whether to discontinue certain models of automobiles.

FedEx must decide whether to expand its services into new markets across the globe. Hewlett-Packard must decide what price discounts to offer corporate clients that purchase large volumes of its products.

In an economic downturn, a manufacturer might have to decide whether to eliminate one 8-hour shift at three plants or to close one plant.

CONFLICTING RULE OF BUDGET

- Demanding unreasonable targets may demotivate the managers.

- Business conditions change upset the budget plan.

- Compare results with adjusted budget to reflect actually operated conditions.

- Sale target is too high and difficult to achieve.

- Arrangement of fund for expansion, but available bank facilities already disbursed.

- Marketing too many new products at the same time is difficult.

- Budget allocated for media is insufficient.

CRITISIM ON BUDGETING

In recent years, criticisms of traditional budgeting have attracted much publicity for instances:

- Focusing on short term financial number.

- Being time consuming

- Producing variances leaving the “HOW” and “WHY” questions unanswerable.

- Achieving the budget even if this results undesirable actions.

Apart from the criticism, budget is alive and important for planning, control and performance measurement.

OUR SERVICES

An independent review of budget is to identify its functionality and basic assumptions/ guidelines under which it has drawn, further, we will see supporting information and evidences for backup support of reported budget.